Learning how to pay off credit card debt—especially $10,000 or more—feels overwhelming. Many people struggle to pay off credit card debt because they don’t have a clear strategy or timeline. But here’s the truth: you can pay off credit card debt faster than you think with the right strategy. Whether you can eliminate your balance in 12 months or 36 months depends on three factors: your interest rate, your monthly payment, and your repayment method.

In this guide, you’ll see real payment plans, exact timelines, and actionable steps to eliminate $10,000 in credit card debt. Use our debt payoff calculator to create your personalized plan and see when you’ll be debt-free.

Let’s break down exactly how to do this.

How Long Does It Take to Pay Off $10,000 Credit Card Debt?

The time to pay off $10,000 depends on your monthly payment and interest rate. Here are real scenarios:

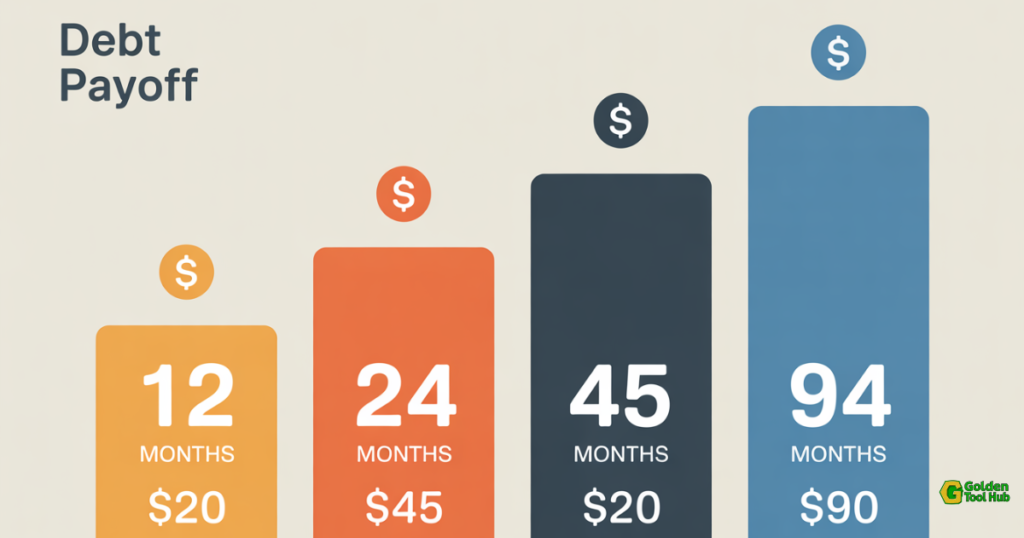

At 18% APR (typical credit card rate):

$200/month = 94 months (almost 8 years), $8,760 in interest

$300/month = 45 months (3.75 years), $3,500 in interest

$500/month = 24 months (2 years), $1,800 in interest

$833/month = 12 months (1 year), $880 in interest

At 24% APR (high-interest card):

$200/month = Never paid off (barely covers interest!)

$300/month = 56 months (4.7 years), $6,800 in interest

$500/month = 26 months (2.2 years), $2,900 in interest

$833/month = 13 months (1.1 years), $1,400 in interest

The key to successfully paying off credit card debt is understanding these numbers upfront. When you can see exactly how your interest rate and payment amount affect your timeline, you can make informed decisions about how aggressively to pay off credit card debt.

Use our credit card payoff calculator to see your exact timeline based on YOUR interest rate and payment amount.

The shocking truth: If you only pay the minimum (typically 2% of balance), you’ll be in debt for 15-20 years and pay over $14,000 in interest on your original $10,000 debt.

Step-by-Step Guide to Pay Off Credit Card Debt ($10,000 Example)

Step 1: Stop Using the Cards

You cannot pay off debt while simultaneously adding to it. This is the hardest step psychologically but the most important mathematically.

Action: Remove credit cards from your wallet. Freeze them in ice. Delete saved payment info from websites. Use debit or cash only until you’re debt-free.

Exception: Keep ONE card with low balance for emergencies, but define “emergency” strictly (car breakdown = yes, new shoes = no).

Remember: You cannot simultaneously pay off credit card debt while adding new charges. The math doesn’t work.

Step 2: Calculate Your Exact Numbers

Before you can pay off credit card debt effectively, you need three numbers::

- Total balance across all cards: Add up everything

- Weighted average APR: If you have multiple cards with different rates

- Available monthly payment: How much can you realistically pay?

Use the debt payoff calculator to input these numbers and see your debt-free date.

Example:

- Total debt: $10,000

- Average APR: 19.5%

- Monthly payment: $400

- Result: Debt-free in 30 months, $1,900 total interest

Step 3: Choose Your Payoff Strategy

Debt Avalanche (Save Most Money):

Pay minimums on all cards, put extra toward highest interest rate first.

Best for: Disciplined people motivated by math

Savings: $500-1,500 more than snowball

Debt Avalanche 📉

Pay minimums on all cards, put extra toward the highest interest rate first. This saves the most money mathematically.

Debt Snowball ❄️

Pay minimums on all cards, put extra toward the smallest balance first. This provides psychological wins.

Both methods work to pay off credit card debt—the best one is whichever keeps you motivated and consistent over time.

Debt Snowball (Best for Motivation):

Pay minimums on all cards, put extra toward smallest balance first.

Both methods work to pay off credit card debt—the best one is whichever keeps you motivated and consistent over time.

Best for: People who need quick wins to stay motivated

Benefit: See cards paid off faster (psychological boost)

My recommendation: If all your cards are above 18% APR, use avalanche. If rates are similar, use snowball for the motivation boost.

Use our debt payoff calculator to model both scenarios and see which saves you more.

Step 4: Find Extra Money

The fastest way to pay off credit card debt is to increase your monthly payment. Every extra dollar accelerates your timeline and saves you interest.

The key to paying off credit card debt faster is finding extra money in your budget. Even an additional $50/month can shave months off your timeline. Paying off $10,000 faster means finding extra money. Here are proven tactics:

Immediate (This Week):

- Cancel unused subscriptions ($20-100/month)

- Sell unused items on Facebook Marketplace ($200-500 one-time)

- Pick up one weekend shift or gig ($100-300/month)

Short-term (This Month):

- Negotiate lower insurance rates ($30-80/month)

- Refinance high-interest debt to personal loan (if qualified)

- Ask for balance transfer to 0% APR card (12-18 months no interest)

Long-term (Next 3 Months):

- Side hustle ($200-800/month)

- Ask for raise at work

- Downgrade car payment (if applicable)

Every extra $50/month saves you 3-6 months and hundreds in interest.

Step 5: Negotiate Lower Interest Rates

Call your credit card companies and ask for a rate reduction. Here’s the script:

“Hi, I’ve been a customer for [X years] and have made on-time payments for [X months]. I’m working to pay off my balance and would like to request a lower interest rate. Can you reduce my current rate of [X%]?”

Lowering your interest rate makes it easier to pay off credit card debt because more of each payment goes toward your actual balance instead of interest charges.

Success rate: 50-70% if you have 6+ months of on-time payments

Potential savings: 3-5% APR reduction = $300-600 over life of debt

Even a small rate drop makes a big difference. Use the calculator to see how much a 3% rate reduction saves you.

Step 6: Track Your Progress

Watching your balance decrease is incredibly motivating.

Monthly tracking:

- Update your balance in the debt payoff calculator

- Calculate percentage paid off use our percentage calculator

- Celebrate milestones (25% paid, 50% paid, 75% paid)

Visual tracking:

- Create a bar chart showing decreasing balance

- Mark your projected debt-free date on calendar

- Set phone reminder for the day you’ll be debt-free

Why Most People Struggle to Pay Off Credit Card Debt

Before diving into solutions, let’s talk about why paying off credit card debt is so hard:

The Minimum Payment Trap: Banks design minimum payments to keep you in debt for decades. At $10,000 balance with 20% APR, minimum payments mean 15+ years of payments.

Compound Interest: Every month you carry a balance, interest compounds. You’re not just paying interest on your original debt—you’re paying interest on interest.

Psychological Exhaustion: When your balance barely moves despite regular payments, it’s demoralizing. Many people give up before seeing progress.

Solution: Use our debt payoff calculator to see exactly how much of each payment goes to interest vs. principal. Understanding the numbers is the first step to beating them.

Real Examples: How to Pay Off $10,000 Credit Card Debt in 12-36 Months

Seeing real-world examples of how others managed to pay off credit card debt helps you understand what’s actually achievable. Here are three different approaches:

Example 1: Aggressive 12-Month Plan (Sarah, 29)

Starting situation:

- Total debt: $10,000

- APR: 20%

- Monthly income: $4,500

- Available for debt: $850/month

Strategy:

- Stopped all discretionary spending

- Picked up weekend bartending gig

- Used debt avalanche method

Results:

- Paid off in 12 months

- Total interest: $1,100

- Debt-free date: December 2026

Key to success: Extra income from side gig ($300/month) made the difference.

Example 2: Balanced 24-Month Plan (Marcus, 35)

Starting situation:

- Total debt: $10,000

- APR: 18%

- Monthly income: $5,200

- Available for debt: $450/month

Strategy:

- Negotiated rate down to 15%

- Used debt snowball for motivation

- Maintained emergency fund while paying debt

Results:

- Paid off in 24 months

- Total interest: $1,650

- Debt-free date: January 2028

Key to success: Rate negotiation saved $400 in interest.

Example 3: Slower 36-Month Plan (Jamie, 42)

Starting situation:

- Total debt: $10,000

- APR: 22%

- Monthly income: $3,800

- Available for debt: $320/month

Strategy:

- Balance transfer to 0% APR card (18 months)

- Paid $555/month during 0% period

- Dropped to $300/month after promo ended

Results:

- Paid off in 32 months

- Total interest: $890 (saved $2,500 with balance transfer)

- Debt-free date: September 2028

Key to success: 0% balance transfer card was game-changer.

Calculate YOUR personalized plan: Use our free debt payoff calculator

Common Mistakes When Trying to Pay Off $10,000 Credit Card Debt

Knowing what NOT to do is just as important as knowing the right steps when you’re trying to pay off credit card debt. Avoid these five critical mistakes:

Mistake #1: Only Paying the Minimum

Result: 15-20 years in debt, $14,000+ in interest

Mistake #2: Not Having a Plan

Result: Paying randomly, no clear end date, high chance of giving up

Mistake #3: Taking On New Debt While Paying Off Old Debt

Result: Balance never decreases, endless cycle

Mistake #4: Not Tracking Progress

Result: Lose motivation, forget how far you’ve come

Mistake #5: Choosing Wrong Payoff Method

Result: Get discouraged, quit before finish line

Avoid these mistakes by using our debt payoff calculator to create a clear, realistic plan you can actually stick to.

Balance Transfer vs Personal Loan to Pay Off Credit Card Debt

If your goal is to pay off credit card debt faster and save money on interest, you have more options than just making bigger payments. Two popular alternatives can dramatically reduce your costs:

Balance Transfer Card (0% APR for 12-18 months):

✓ Best for: People who can pay off most/all debt during 0% period

✓ Savings: $1,500-3,000 in interest

⚠ Watch out for: 3-5% transfer fee, high APR after promo ends

Example: $10,000 debt, 0% for 18 months

- Pay $555/month = debt-free before promo ends

- Fee: $300-500

- Interest saved: $2,500+

- Net savings: $2,000+

Personal Loan (Fixed rate 8-12%):

✓ Best for: Lower rate than credit cards, fixed payment

✓ Savings: $500-1,500 in interest vs credit cards

⚠ Watch out for: Origination fees, credit score requirement

Example: $10,000 loan at 10% for 3 years

- Monthly payment: $323

- Total interest: $1,628

- vs. credit card at 20%: $3,500 interest

- Savings: $1,872

Use the debt payoff calculator to compare all three scenarios: current credit cards, balance transfer, or personal loan.

CONCLUSION

Learning how to pay off credit card debt is just the beginning. Successfully paying off credit card debt—even large balances like $10,000—requires a clear strategy and consistent action. Whether it takes 12 months or 36 months depends on your situation, but having a roadmap makes all the difference.

Your next steps to pay off $10,000 credit card debt:

- Calculate your exact timeline with our free debt payoff calculator

- Choose debt avalanche or snowball method

- Find $50-200 extra per month in your budget

- Negotiate lower interest rates with your card companies

- Track your progress monthly

Remember: Every extra dollar you pay saves money in interest and gets you debt-free faster. Start today.

Dealing with debt while watching family members succeed financially? You’re not alone. Check out our guide: “When Your Relatives Are Buying Their Third House and You Can’t Afford Rent” for emotional support and financial strategies.